Selling a House in Foreclosure in Michigan

- Published on

- 13 min read

-

Cheyenne Wiseman EditorClose

Cheyenne Wiseman Editor

Cheyenne Wiseman EditorClose

Cheyenne Wiseman EditorCheyenne Wiseman is an Editor at HomeLight. Previously, she worked as a writer for Static Media (Mashed.com and Chowhound.com) and as an editor for CBR.com. Cheyenne holds a bachelor’s degree in English from UC Davis. She has more than five years of experience writing and editing on topics including real estate, financial advising, and pharmaceuticals.

If you’re a Michigan homeowner facing foreclosure, the situation can feel stressful and overwhelming, especially if deadlines are approaching. You may be wondering about your options for selling a house in foreclosure in Michigan.

In many cases, homeowners can still sell before the foreclosure process is complete. The key is understanding how Michigan’s foreclosure rules work, how much time you may have, and which selling path makes the most sense for your situation.

Below, we’ll explain what foreclosure typically looks like in Michigan, how long the process can take, and whether selling before the auction date could help you avoid longer-term financial setbacks.

Get a Cash Offer For Your Michigan Home in 24 Hours

With Simple Sale, you can receive a no-obligation all-cash offer in 24 hours and close in as few as 7 days. No showings. No repairs. You’ll also get an estimate of what your home might sell for using a top-rated Michigan agent.

According to data from ATTOM, approximately 300,000 foreclosures occur in the U.S. each year, and that number is on the rise. Based on an end-of-year report, the statewide foreclosure rate in Michigan is 1 in every 3,419 housing units.

The state also saw a 51% increase in zombie foreclosures, with vacant homes in foreclosure rising from 55 to 83. In lower-priced markets like Detroit, where median home prices are around $100,000, some homeowners may have fewer options once they fall behind.

Can you sell a house in foreclosure in Michigan?

In most cases, you can sell your Michigan home while it’s in foreclosure, as long as the foreclosure sale hasn’t yet taken place.

Many homeowners are surprised to learn that they retain ownership of the property throughout most of the foreclosure process. That means you generally have the right to sell the home, pay off the loan, and stop the foreclosure before the final sale date.

“I would let homeowners know there are a lot of options, and I’m here to help you with them. It’s not actually the end of your story if you are facing foreclosure,” says Bethany Brokaw, a top-performing Michigan real estate agent with more than 15 years of experience.

The sooner you explore selling, the more flexibility you typically have regarding price, buyers, and outcomes.

How foreclosure works in Michigan

Michigan is primarily a non-judicial foreclosure state, which means most lenders can foreclose through a process called foreclosure by advertisement instead of filing a lawsuit in court. This often makes the process faster than in states that require court involvement.

“One of the largest misconceptions that people tend to have is that once they are foreclosed on, they are foreclosed on. Basically, meaning that once they get that notification in the mail and the phone calls start happening, they truly believe that ‘I’m done. I have no other options. I need to leave my house. They’re going to kick me out,’ and most people end up walking away from their home,” says Brokaw.

In Michigan, foreclosure typically follows these steps:

- You fall behind on mortgage payments.

- Your lender contacts you about missed payments and possible ways to avoid foreclosure.

- If the issue is not resolved, the lender initiates foreclosure proceedings after about 120 days of delinquency.

- A sheriff’s sale date is scheduled and publicly posted.

- Your home is sold at a sheriff’s sale.

- After the sale, you may still have time to sell, refinance, or redeem the home before you have to move out.

In most cases, lenders must wait until you are more than 120 days behind before starting foreclosure. This gives homeowners time to explore options such as a loan modification, repayment plan, or selling the home.

Michigan also has a post-sale redemption period. For most homeowners, this lasts about six months, though it can be shorter or longer depending on the property and loan. During this time, many homeowners can remain in the home while they work out their next steps.

How long does foreclosure take in Michigan?

Foreclosure timelines in Michigan can vary, but the process often takes several months from the first missed payment to the sheriff’s sale. In most cases, lenders cannot begin formal foreclosure until you are more than 120 days behind on payments, and the sale must be publicly noticed before it can move forward.

Even after the sheriff’s sale, many Michigan homeowners still have a redemption period. In most cases, this lasts about six months, giving you time to sell the home, pay off the balance, or make other arrangements. Some properties may qualify for a longer redemption period.

While this may sound like plenty of time, important deadlines can still come quickly once the process is underway.

“The timeline can vary based on the particular mortgage lender. However, once the foreclosure process starts, homeowners could have anywhere from, at the absolute minimum, seven months to a maximum of even around two years or so. Every lender is different in their speed of when they actually file the foreclosure to get it to share of sales,” Brokaw explains.

If you’re already behind on payments or have received legal notices, speaking with a local expert as soon as possible can help you understand how much time you may have and what options could still help you avoid foreclosure, including selling before or during the redemption period.

What happens if you sell before foreclosure is finalized?

Selling your Michigan home before the foreclosure sale may stop the process and help you avoid more serious long-term financial damage. In most cases, sale proceeds first go toward paying off your remaining mortgage balance, along with any accrued interest, fees, and foreclosure-related costs. Once the loan is paid, the foreclosure is typically canceled.

Taking action sooner may also lessen the hit to your credit compared with a completed foreclosure, which can stay on your credit report for years. And if your home sells for more than what you owe, you may be able to keep the remaining equity to help with your next move.

“In a perfect scenario, anyone who’s facing foreclosure would call a real estate professional who’s familiar with this process right away. Their worst-case scenario is that the foreclosure is filed. However, they can still call a real estate professional even after that, because we can still save a lot of things for them,” says Brokaw.

If your expected sale price won’t fully cover the loan balance, a short sale may still be an option with lender approval. That’s another reason to explore your choices as early as possible.

Option 1: Selling with a top Michigan real estate agent

For homeowners who still have enough time before foreclosure, working with an experienced Michigan real estate agent is often the best way to maximize the sale price.

A knowledgeable local agent can:

- Set a competitive price based on current Michigan market conditions

- Market the property widely to attract serious buyers

- Negotiate with buyers and, if needed, coordinate with the lender on a short sale

- Keep the transaction moving to meet foreclosure-related deadlines

“It’s very, very important to use someone already familiar with the foreclosure process in Michigan. Because when you are either facing foreclosure or foreclosure has been filed, the timelines are extremely imperative,” says Brokaw.

Because timing matters, connecting with a proven agent early can make a big difference. HomeLight’s free Agent Match platform analyzes more than 27 million transactions and thousands of reviews to identify top-performing Michigan agents based on your needs. To get started, enter a few details about your home and timeline.

A top Michigan agent can help you make informed decisions and avoid costly delays.

How fast can you sell with an agent in Michigan?

The timeline for an agent-assisted sale in Michigan depends on your pricing strategy, home condition, location, and buyer demand. On average, homes in Michigan spend about 51 days on the market from listing to signed contract. However, a well-priced home in good condition may attract buyers much faster.

If you’re on a tight timeline, an experienced agent may be able to help move the process along and improve your chances of selling before key foreclosure deadlines.

If your situation is more urgent, it may also make sense to compare this route with faster options, such as selling to a cash buyer.

Consult With a Top-Performing Michigan Agent

Homelight’s free Agent Match platform can connect you with top-performing, trusted real estate agents in your Michigan market. Our data shows that the top 5% of agents sell homes more quickly and for up to 10% more than the average agent.

Option 2: Selling for cash to avoid foreclosure in Michigan

If your foreclosure timeline is tight, selling your Michigan home for cash may offer a faster and more predictable way forward. Cash buyers, including investors and Michigan house-buying companies, often purchase homes “as is” and can sometimes close in days or weeks rather than months.

The biggest benefit is speed and certainty. With no buyer financing and fewer contingencies, a cash sale may move quickly enough to help you avoid the foreclosure sale. The tradeoff is that cash offers are usually lower than what you might get through a traditional listing.

“If we are in a rush situation with the timeline, then at that point, we would most likely pursue a cash-only sale. Usually, it is an investor purchasing. We will sometimes have an actual homeowner purchasing, but most of the time, it will be an investor,” says Brokaw.

How much will a Michigan house-buying company pay?

Use the Cash Offer Comparison Calculator below to get a rough idea of how a cash offer in Michigan might compare with an agent-assisted sale, depending on your selling method and whether you work with a top agent.

As the calculator shows, your cash offer may be higher if your Michigan home is in good condition. But if you’re facing foreclosure, you may not have the time, money, or energy to make repairs. In situations where speed matters most, a fast cash offer can provide needed certainty and relief.

Examples of cash home buyers in Michigan

Homeowners looking for a quick sale will often come across local and regional “We Buy Houses” companies. These buyers typically focus on fast closings and minimal seller prep. A few examples serving Michigan include:

- M1 Home Buyers (see customer reviews)

- Mitten Home Buyer (see customer reviews)

- Michigan Houses For Cash (see customer reviews)

- Swift House Buying (see customer reviews)

- Connect Home Buyers (see customer reviews)

- Sell Dave Your House (see customer reviews)

Because every cash home-buying company in Michigan has its own pricing formula, closing timeline, and contract terms, it’s smart to compare multiple offers before making a decision.

You’ll also want to vet any cash-for-homes company carefully. That said, there is a way to move quickly while still working with a trusted, established buyer.

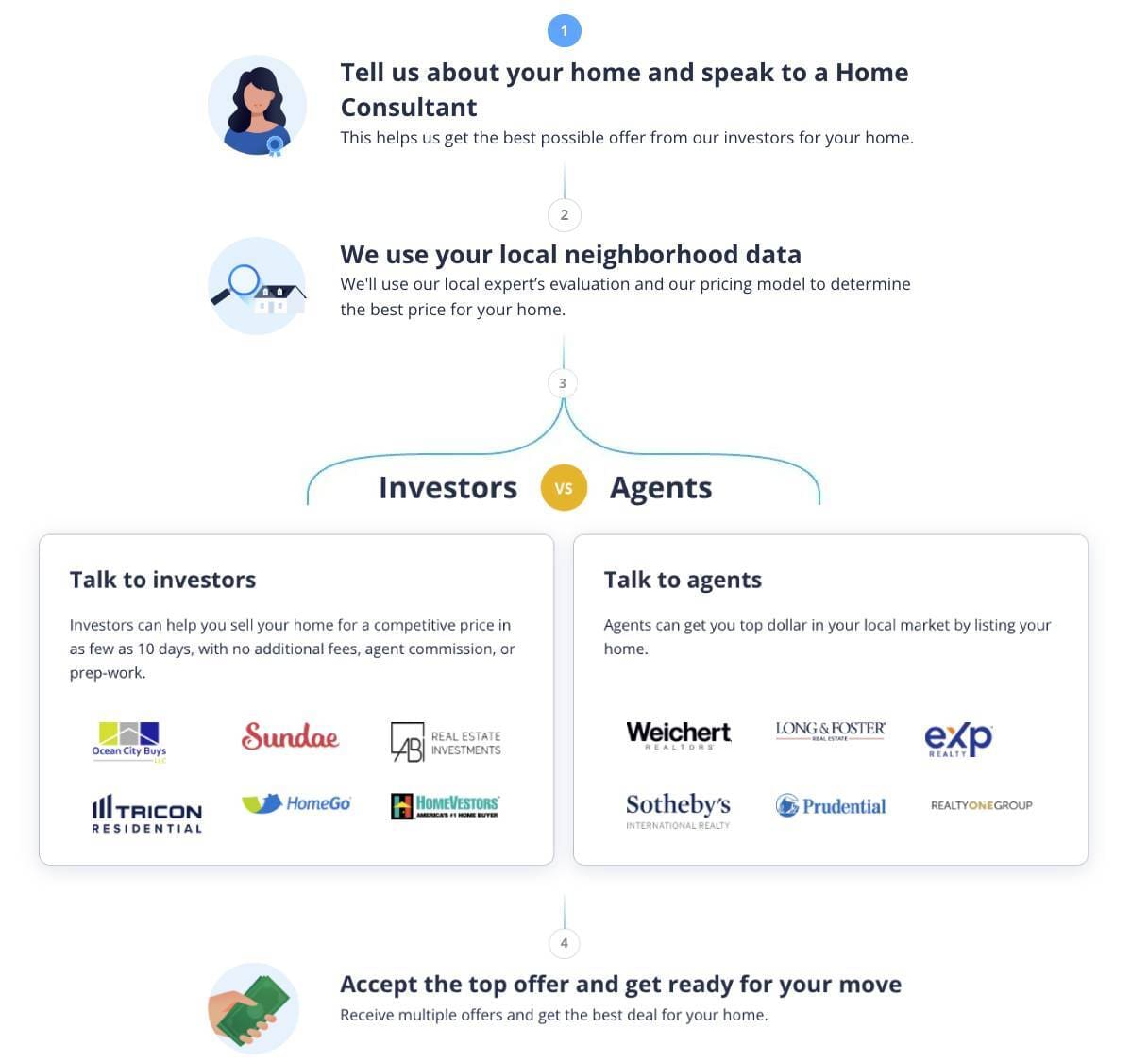

Selling your house through HomeLight Simple Sale

HomeLight’s Simple Sale platform connects you with the largest network of vetted cash buyers in the country, including trusted buyers in Michigan. With Simple Sale, you can receive a no-obligation cash offer in 24 hours and close in days, not months.

Through Simple Sale, Michigan homeowners can:

- Request a no-obligation all-cash offer

- Sell the home “as is,” without repairs or showings

- Choose a flexible closing timeline that fits their situation

Here’s the four-step Simple Sale process:

HomeLight’s Simple Sale can provide cash offers for Michigan homes in almost any condition. To get started, fill out this short questionnaire.

Here are a few examples of what HomeLight customers are saying about Simple Sale:

Baohan Wu needed to sell quickly. Through HomeLight’s Simple Sale platform, Wu requested an all-cash offer and sold his home in about 24 days from start to finish.

Learn about Wu’s Simple Sale experience in the video below:

A fast, all-cash purchase offer isn’t right for everyone. But if you’re facing foreclosure in Michigan and want a faster, more predictable path, Simple Sale may be worth considering. You’ll also see what a top Michigan agent might be able to get for your home, so you can compare both options.

HomeLight maintains an A+ rating with the Better Business Bureau and has a 4.8-star customer review ranking on Google. You can read these and other HomeLight customer reviews at homelight.com/testimonials.

Which selling option is right for your situation in Michigan?

The best way to approach selling a house in foreclosure in Michigan depends on your timeline, how much equity you have, and your overall financial goals.

In general:

- Working with a Michigan agent may make sense if you still have time and want the best chance at a higher sale price.

- Pursuing a cash sale may be the better fit if speed, certainty, and avoiding the sheriff’s sale are your top priorities.

“Even if a foreclosure is coming, I highly recommend reaching out to an agent first because a lot of times, as long as it’s an experienced agent, they’ll be able to advise you on the cash sale versus going on the market. Sometimes we go on the market to get a cash sale because we can reach many more investors on the market,” Brokaw says.

Comparing both options side by side can help you make a clearer decision without feeling rushed.

Talk to a Michigan expert before the foreclosure clock runs out

If you’re facing foreclosure in Michigan, exploring your options sooner can preserve more flexibility. Even a short conversation with a knowledgeable local professional can help you better understand your timeline, likely sale price, and next steps.

HomeLight can connect you with a trusted Michigan agent through Agent Match or help you explore a fast cash offer through Simple Sale. With Simple Sale, you’ll also see what a top agent may be able to get for your home, so you can compare both paths before deciding.

“If someone knows they’re on their way to foreclosure, the best thing they can do is reach out to a real estate professional right away. Because if we can get the house sold and on the market prior to the foreclosure being filed, their credit is still saved, which means you can buy a house and get pre-approved for a mortgage in the future,” Brokaw advises.

Foreclosure can feel overwhelming, but with timely action and the right support, many Michigan homeowners can still sell, protect their finances, and move forward.

Header Image Source: (Nikunj Singh/ Unsplash)

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.